Turkey's policy hopes dashed as Erdogan wins presidency; and could travel spend keep Europe’s luxury goods firms in a sweet spot?

Turkey's policy hopes dashed as Erdogan wins presidency; and could travel spend keep Europe’s luxury goods firms in a sweet spot?

13 June 2023

Turkey: Hope Over Experience

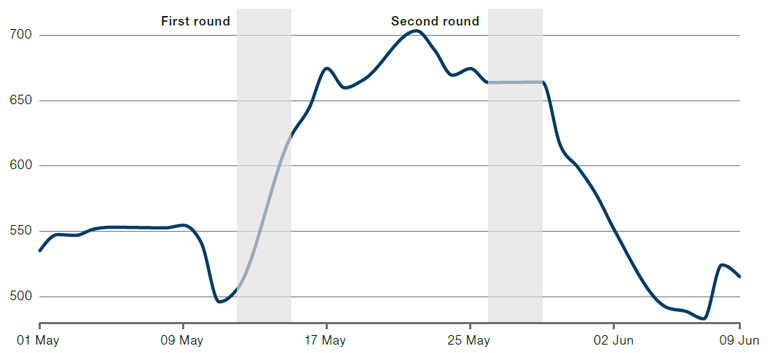

As expected, Turkish President Recep Tayyip Erdogan won his re-election for another term on 28 May, defeating opposition leader Kemal Kilicdaroglu. Turkey’s five-year credit default swaps (‘CDS’) initially sold off after the first round (Figure 1) as investors were disappointed by the strong showing of Erdogan in the results, which would imply a continuation of the same unorthodox economic policies of the past. Spreads started recovering, however, when Erdogan began hinting of a move back to more orthodox policies by considering Mehmet Simsek for the position of Treasury and Finance Minister.

Figure 1. Turkey Five-Year Credit Default Swaps

Source: Man Group, Bloomberg.

Simsek is considered a technocrat, with experience on Wall Street and roles as Minister of Economy and Deputy Prime Minister in previous Erdogan governments. In his new cabinet, Erdogan assigned Simsek to the ministry of Treasury and Finance which led to a further rally in Turkish assets.

On his first day, Simsek promised to bring “accountability and transparency” and turn the dial back towards rational policies. In addition, Hafize Gaye Erkan, who is US-educated and a former employee of Goldman Sachs, has been appointed at the helm of the central bank. She may well have a stellar resume, but has no monetary policy or central bank experience.

Even though President Erdogan seems to have shifted when it comes to economic policy, we see the challenges facing Turkey to be much bigger for the following reasons. First, official inflation is above 40% YoY when interest rates are just 8.5%. Will Simsek and his team have the autonomy to freely hike interest rates sufficiently to restrictive levels and slow down the economy enough to tackle inflation?

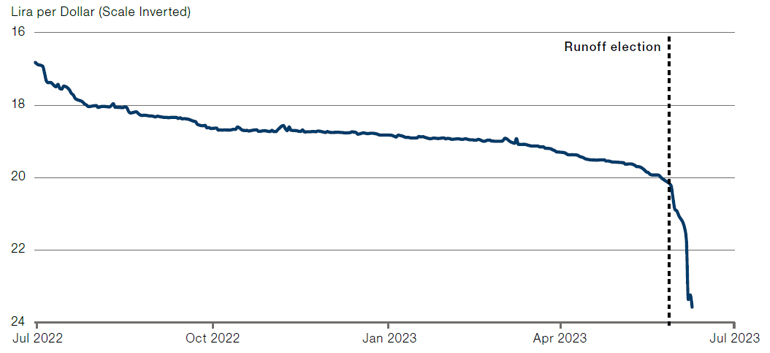

Second, the current account deficit is running at a pace of $50 billion per year. The central bank has borrowed dollars from local banks (and other friendly countries) to prop up the value of the lira, which weakened sharply after the election (Figure 2). Central bank net reserves (excluding off-balance-sheet foreign exchange swaps) are deeply negative. There is only an estimated $20-30 billion left in liquid FX reserves after an average $4 billion a month1 was spent prior to the election this year.

Figure 2. The Turkish Lira Has Weakened Sharply

Source: Man Group, Bloomberg.

After 28 May, the lira started selling off. The decline accelerated on 7 June (with the currency weakening by almost 7%) as state banks stopped selling dollars. Bloomberg reports that state banks had resumed selling dollars to slow down the lira’s devaluation suggest that Simsek might not have the full autonomy to front load the adjustment. Investors responded by putting further pressure on external spreads, resulting CDS spreads moving higher the following day on 8 June (Figure 1).

Third, there is close to $130 billion in the FX-protected deposits scheme, according to Bloomberg data, which places a large fiscal burden on the government as the lira needs to, and continues to, depreciate. It will be challenging for Simsek and his team to unwind this without pushing local depositors into buying more dollars.

Finally, and most importantly, a local election is scheduled for early next year. President Erdogan has been trying to regain the control of the Istanbul municipalities. As a result, it may not be too long before he loses his patience, as we have seen it many times before, and do an about-turn to unorthodox policies once more to secure his party victory. For investors who went long on the back of Simsek, this could be the triumph of hope over experience.

A High Price for Luxury Goods

One area of the equity market that has continued to shine thus far in 2023 is the high-quality European luxury goods sector. Having significantly beaten the MSCI Europe (ex UK) index this year, the sector retreated sharply on 23 May despite there not being any material stock-specific catalysts. The sell-off coincided with a luxury goods conference held in Paris, which created apprehension for investors that US consumer demand may be softening, while new Covid cases in China created jitters about the impact of demand growth from Asia.

However, analysis of the drivers of luxury goods consumption shows that for the true higher-quality companies, at least, their appeal to their high-net-worth clientele has not dimmed and so their higher valuations may well be justified.

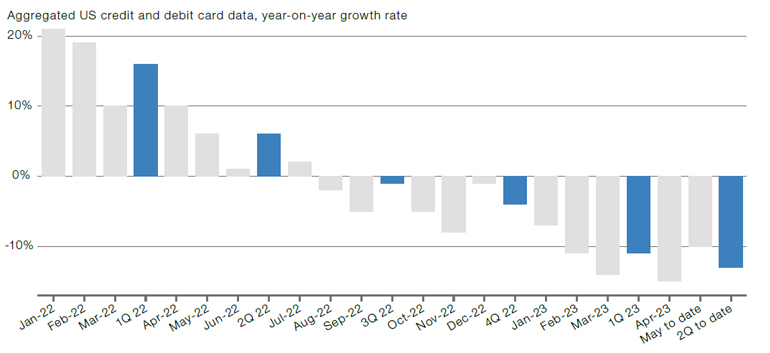

US aggregated credit-and debit-card data for luxury goods spend is down 13% in the quarter to date, as shown in Figure 3, but this has not translated into earnings growth falling off a cliff for high-quality luxury names, despite the importance of wealthy Americans to their businesses. For example, in the US, Hermès still managed to grow by 19% in constant currency in the first quarter this year, with strong growth in underlying volumes despite putting through low single-digit price increases.2 It is also worth noting that the relative strength of the US dollar has affected domestic US spending, as Americans have opted to take advantage of their strong currency and take their luxury shopping in Europe instead.

Figure 3. US Luxury Fashion Spending Is Slowing

Source: Consumer Edge, Bank of America-Merrill Lynch; as of 29 May 2023.

China, another key market for luxury items, is reopening and domestic travel has shown a resurgence. Data from Global Blue, a provider of tax-free shopping, shows that there is a strong recovery for Chinese travel intentions, with their survey of affluent shoppers finding 83% of shoppers are willing to travel internationally, to other regions in Asia and to Europe.3 Considering that some air routes have only very recently been reopened with mainland China, there is capacity for further recovery in pent-up luxury spend by affluent Chinese.

The average affluent shopper surveyed spent €2,500 in 2019 but €3,300 last year, an increase of 1.3 times. However, the higher-spending consumers spend vastly more on shopping trips, with the top tier spending €134,800 in 2022, 2.6 times more than three years ago, and proving to be more resilient in their spending than lower-income bands. This feeds into the performance of those companies that have higher exposure to high-net-worth individuals, rather than those catering more to the mass affluent. It is estimated that 2% of these ‘VICs’ (Very Important Customers) accounted for 40% of total luxury spend last year,4 highlighting the significance of this small but financially important segment.

With these drivers seemingly firmly in place, the high-quality luxury goods names may be more resilient and deserving of their valuations than the headlines in May suggested

1. Source: Bloomberg, Goldman Sachs.

2. Source: Hermès International Quarterly information report as at the end of March 2023.

3. Source: Global Blue ‘Willingness to travel’ survey for May 2023.

4. Source: Global Blue report, ‘From Actions to Insights – A blueprint for capturing the return of Chinese luxury shoppers’, 30 March 2023.

With contributions from: Ehsan Bashi (Portfolio Manager, Man GLG) and William Burke-Nash (Equity Analyst, Man GLG).

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.