Execution within credit trading has undergone multiple turnarounds in recent years. In this paper, we explain what the dramatic changes mean for investors.

Execution within credit trading has undergone multiple turnarounds in recent years. In this paper, we explain what the dramatic changes mean for investors.

June 2023

The future of credit execution is quantitative.

Introduction

The greatest barriers to systematic approaches breaking through in credit have traditionally been execution and the ability to model transaction costs and liquidity within decades-old manual processes. The past few years, however, have broken down those barriers through the rapid evolution from voice trading to portfolio trading and electronic trading. In our view, these are clear signs that the future of credit execution is quantitative.

Indeed, when we first wrote on this topic for Man Institute in February 2021, we observed:

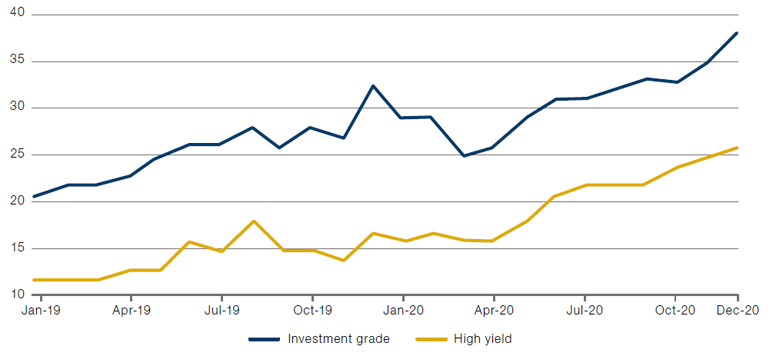

“What is inelegantly referred to as the ‘electronification’ of the credit markets has been a halting process, but appears finally to have gained momentum in the past few years. As the chart below shows, the percentage of trades being executed on electronic platforms has grown substantially in recent years, with MarketAxess’s Open Trading platform alone securing a sizeable proportion of this. While investment-grade credit remains more active than high yield or distressed, we expect a continuation of this move away from cumbersome over-the-counter trading towards more efficient electronic trading and ‘straight-through processing’ (STP).

Taking this one step further, more sophisticated market makers are investing heavily in algorithmic market making, where dealers continuously stream quotes directly to the market. This is a paradigm shift relative to MarketAxess’s predominantly Request for Quotation (RFQ)-based process, giving credit investors more real-time price discovery and improved liquidity in corporate bonds.”

Figure 1. Percentage Share of Electronic Bond Trading, 2018-2020

Source: Greenwich MarketView; as of 27 December 2020.

In this paper, we describe the trends we have seen since then and discuss what they mean for investors.

Rise and Fall

The first revolution became apparent two years ago. For most of its history, credit trading had been conducted primarily through telephone calls or electronic messages with sell-side dealers. 2021 then became, in our view, the year of portfolio trading (Figure 2). We found that orders attracted high fill rates as competition for trades proliferated, not only among what we would consider tier-one counterparties but also those in the second tier, with aggressive pricing offered. We attribute this to a combination of the growth of bond ETF trading and the advances made by algorithmic market-making desks on fixed income. These developments helped dealers become more comfortable in their ability to price debt securities in near real time and in greater size, initially in investment grade and then eventually within high yield too. The majority of our order flow duly switched from voice based to portfolio trading.

Figure 2. Tradeweb Platform High Yield Portfolio Trading

Problems loading this infographic? - Please click here

Source: Tradeweb; as of Q4 2022.

The information contained herein is highly confidential and some or all of it may constitute material, non-public information under applicable securities laws. This information must be kept strictly confidential, may not be disclosed or distributed to anyone without the express written consent of Tradeweb Markets LLC, and may only be used as expressly permitted by any applicable non-disclosure, customer, or other written agreement with Tradeweb.

Yet 2022 saw the pattern revolve again, somewhat surprisingly, as transaction costs for portfolio trading generally increased through the first half of the year. It appeared that after significant competition as participants tried to gain market share, ultimately pricing backed off. The new market environment of higher volatility and quantitative tightening may also have left dealers inclined to commit less of their balance sheets to bond trading. The loss of customised baskets for the ETF creation/redemption process is likely to have been another aggravating factor.

One of the venues where pricing and liquidity held up best last year was electronic execution.

One of the venues where pricing and liquidity held up best last year, however, was electronic execution (Figure 3). Originally, we would have expected the tipping point for switching to electronic execution to come as it won the majority of the market share for trading. In fact, this point seems to have been reached sooner than that and has instead been based on electronic venues delivering best execution from a transaction-cost perspective by slicing up trades more efficiently. We have therefore moved from having roughly 30% of our order flow in high yield and 60% in investment grade going through electronic venues, to over 90% of our order flow going through electronic-trading venues.1

Figure 3. Growth of Electronic Trading, 2019-2022

Problems loading this infographic? - Please click here

Source: Greenwich MarketView; as of 31 December 2022.

We believe all of this is a genuine game changer for quantitative investing in credit.

In addition, the options for electronic trading are becoming more diversified (Figure 4). We have noted a particular expansion of session-based trades (more commonly known as dark pools or IOI matchers) and live/streaming prices/CLOB protocols.

We believe all of this is a genuine game changer for quantitative investing in credit. Two of the key challenges for such systematic techniques are having a high certainty of execution and having a relatively good sense of the likely transaction costs, as quantitative approaches depend on being able to model accurately which securities can be traded and at what cost.

Figure 4. Credit Trading Volume by Protocol

Problems loading this infographic? - Please click here

Source: Greenwich MarketView; as of 31 December 2022.

The most salient implications of these developments relate to transaction costs and liquidity.

Adapting to the New Environment

As quantitative credit investors, we believe the most salient implications of these developments relate to transaction costs and liquidity. These costs are critically important in systematic credit, especially when spreads are tight and high costs can offset a trade’s potential profitability. Liquidity modelling is essential too: an optimised portfolio is not optimal if you can’t trade it. Furthermore, unfilled orders may create unintended and potentially unmodelled risk exposures in the portfolio.

Historically, a dearth of data made such cost and liquidity models challenging: there are fewer trades in bonds than in equities, with much less well-defined intraday reference prices; and liquidity in fixed income has tended to be less commoditised than in equities, with trades more contingent on relationships. These two features of the market also complicate analysis of the probability of filling orders, given the time-varying nature of bond liquidity and credit’s significant illiquid tail.

The greater use of electronic trading assists us on all these fronts, and accordingly we enhanced our cost models and implementation processes last year. With over 90% of our order flow now executed on electronic venues2, we have for example been able to make more frequent, smaller trades than was previously possible.

It has also helped us trade around market imbalances. These tend not to occur in highly liquid asset classes, but in credit it is not uncommon to have multiple participants trying to trade in the same direction. When so many investors are trying to sell or buy at the same time, liquidity providers can struggle to digest the volume. Electronic venues give us greater insight into these imbalances – such as realised prints, bid/ask spreads, or trades that were attempted but not executed – and thus greater confidence in identifying and quantifying liquidity and costs.

In our view, this progress towards fast electronic execution – and the associated granularity on costs, liquidity, and order flow – is reaching the sweet spot of ideal conditions for any quantitative or systematic investment approach. To deliver on the potential, however, we believe quantitative credit investors will need to be supported by well staffed and experienced trading teams with algorithmic execution in their DNA. This is rarer than it perhaps should be, given that many large fixed-income institutional investors have relied on voice trading for decades.

Case Study: RFQs

Over the past year, intense investment by the sell side and the growth of algorithmic trading desks have greatly increased RFQ responses. Parallel growth on the buy side and the development of systematic responses to all-to-all (A2A) enabled RFQs have added to the response rate and stirred up even more liquidity.

Reflecting this progress, RFQ analysis has become an increasingly important aspect of our order routing process. We can see whether a security is actually available for RFQ, filtering to only high-quality RFQ participants as well as on the frequency of RFQs, the rate of completed trades, and whether a given trade size is digestible in RFQ form. Identifying recent market imbalances further aids order routing optimisation, drawing on other pre-trade analysis elements to produce a final routing instruction.

The vast majority of our trades are now sent as RFQs, leading to significant savings in transaction costs versus portfolio trades. In our view, it is of vital importance to be smart pre-trade; there will always be some form of outliers in credit, but if we can identify them quickly we can more efficiently route trades to proper venues with the “liquidity sweet spot” in mind.

Conclusion

From voice based to portfolio trading and electronic venues, each method of buying and selling credit has competed fiercely for market share. 2021 was the year of portfolio trading; 2022 was the year of electronic trading. Interestingly and perhaps intuitively, though, some of the biggest jumps in electronic trading have come during the most stressful times in credit trading, such as 2020 and 2022. A consistent theme of the past few years has been investors preferring electronic trading as a solution during challenging times – and strong growth spurts in electronic venues have been a result.

We believe the maturation of electronic trading over the past year can contribute significantly to the pursuit of alpha.

For systematic credit investors, we believe the maturation of electronic trading over the past year can contribute significantly to the pursuit of alpha, both by helping refine transaction cost modelling and by improving the execution of order flow. Put simply, in an ideal world, less trade friction leads to more opportunity to deliver alpha. Electronic trading reduces that friction materially, in our view.

Of course, the commitment to best execution will continue to require access to all trading venues, so we expect there will always be a time and a place for voice and basket trading. Indeed, a similar evolution occurred in equity markets in the 1990s and early 2000s. That said, credit markets – and quantitative investors in particular – have long been waiting for the moment when electronic trading would take over. We think last year’s evolution in best execution is a tipping point and look forward to the benefits it will ultimately bring clients.

1. Source: Man Numeric; as of 1 May 2023.

2. Source: Man Numeric; as of 1 May 2023.

You are now exiting our website

Please be aware that you are now exiting the Man Institute | Man Group website. Links to our social media pages are provided only as a reference and courtesy to our users. Man Institute | Man Group has no control over such pages, does not recommend or endorse any opinions or non-Man Institute | Man Group related information or content of such sites and makes no warranties as to their content. Man Institute | Man Group assumes no liability for non Man Institute | Man Group related information contained in social media pages. Please note that the social media sites may have different terms of use, privacy and/or security policy from Man Institute | Man Group.